Registered Education Savings Plans

Registered Education Savings Plan is a tax-deferred investment vehicle that allows parents to save for children’s post-secondary education. It’s an excellent way to save money for future education needs of children and you can invest up to a lifetime total of $50,000 per child. An RESP is a tax-deferred savings plan where contributions are not tax-deductible but the income earned on contributions compounds on a tax-deferred basis. Investments inside the registered account grow tax free, meaning there are no taxes on capital gains, interest and dividend payments and any investment income that’s earned within the plan isn’t taxed until it’s withdrawn. Additionally, when you contribute the federal government will also automatically contribute a Canada Education Savings Grant (CESG) of 20% of what you put in, up to $500 per year – to a lifetime maximum of $7,200 over the life of the plan for each child. You may be eligible for an even higher amount of grants depending on your family income .Your child may also be eligible for an additional $2,000 under Canada Learning Bond if your family income is low.

Types of RESP Plans

Individual RESP Plans: Individual plans can only have one beneficiary and there are no restrictions on who can be a beneficiary under these plans. It doesn’t matter who opens the account, as long as both the account opener and beneficiary are Canadian residents. It could be a child’s parent, grandparent or a friend of the family. There are no age limits, so you can even set up an RESP for yourself, your spouse or another adult. Subscribers or plan holders will decide how the money will be invested and when, how much and how often the beneficiary will get payments.

Family RESP Plans: Family Plans can have one or more beneficiaries and each beneficiary must be connected by blood or adoption to each living subscriber under the plan or to a deceased original subscriber. A family RESP can be opened only by parents or grandparents of the children and may be spent on the education of any child in the family. Children, grandchildren, adopted children and stepchildren all are fully eligible to be the beneficiary. If due to some unavoidable circumstances, the eldest child can’t go to post-secondary school, the grant money can be transferred to other beneficiaries and there is no need to split payments evenly among children. Subscribers or plan holders will decide how the money will be invested and when, how much and how often the beneficiary will get payments.

Group RESP Plans: A group plan can only have one single child as the beneficiary, and that child does not have to be related to you. As it’s a group plan and many people are contributing to this plan, the beneficiary shares the pooled earnings of investors with children of the same age. Group plans have more restrictions and rules than other plans. Group Plans are usually offered by non-taxable entities like foundations. Some of the largest providers are Knowledge First Financial (which owns Heritage Education Funds), Canadian Scholarship Trust Plans (CST), and Global Education Trust Plan.

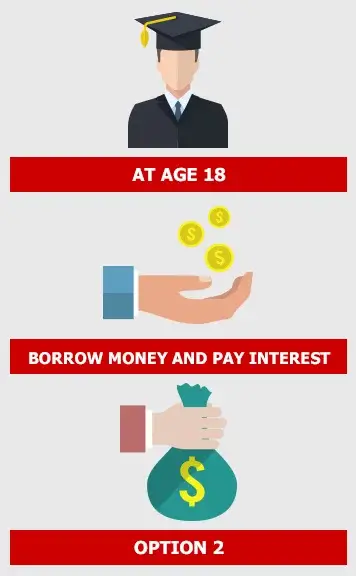

Options to Fund Your Child’s Post-Secondary Education

Education is getting expensive day by day. The average cost of post-secondary education has increased over the past 10 years, and the trend is expected to continue. As a parent you have the following two options to fund your child’s post-secondary education:

| OPTION 1 | OPTION 2 |

|---|---|

| SAVE MONEY AND EARN INTEREST. (Start saving as soon as your child is born and earn interest.) |

BORROW MONEY AND PAY INTEREST. (Borrow money at age 18 and pay interest on it.) |

| 1. Invest in an RESP

2. Get government grants 3. Get Tax sheltered growth 4. Enjoy tax-efficient withdrawals 5. Benefit from the power of compound interest 6. Get peace of mind |

1. Borrow the money

2. Mortgage your home 3. Withdraw from your personal savings 4. Deplete your retirement funds or investments 5. Your child will have to work and earn to pay 6. Take student loans |

A registered education savings plan (RESP) is one of the most effective ways to save for your child’s post-secondary education. An RESP is one of the best investments you can make – Start saving for your child’s education early and contribute regularly to avoid the burden of debt later on. The earlier you start, the more your savings can benefit from the power of compounding. If you start saving when your child is born, the greater timeframe will allow you to save more. Investing in a child’s future is a wonderful gift and a sound investment.

Benefits of Registered Education Savings Plans

RESP is an amazing investment vehicle where if you put in your money for your kids’ post- secondary education, you get free money from the government and that also grows tax-free. While the tax-free growth of your money is the main benefit there are many more benefits of RESPs as follows:

- 1. Encourage Savings: RESP is a government initiative to encourage parents to save for children’s higher education and there are inbuilt safeguards to ensure that money is left to grow. RESPs are a kind of forced savings as there are tax penalties and grant claw backs to discourage the withdrawing RESP funds early by subscribers.

- 2. Government Grants: The government matches 20% of your RESP contributions up to $2,500 each year and up to a lifetime maximum of $7,200. Lower-income families may also qualify for the Canada Learning Bond. These government grants help boost your savings.

- 3. Tax-sheltered Growth: You don’t pay tax on any investment earnings as long as they stay in the RESP. Earnings inside RESPs accumulate tax-free until you withdraw the money. That means your savings can grow faster. Your savings can really grow very big over time.

- 4. A Variety of Investment Options: You have a lot of investment options available as different providers offer different investment options. For Example stocks, bonds, mutual funds, and GICs. You can choose investments that best suit your investment objectives, risk tolerance, and time horizon.

- 5. An Extremely Thoughtful Gift: RESP is a gift of education and parents, grandparents or friends can give the most meaningful gift that keeps on giving.

- 6. Flexible to Use: You can use your RESP savings for a variety of expenses related to your child’s post-secondary education. This includes tuition, housing books, transportation and many other costs.

- 7. Tax Efficient Withdrawals: Your Contributions can be withdrawn by you or by the student tax-free. The educational assistance payments (EAPs) withdrawals are taxed in the hands of your child and not you. Since students tend to have little or no income, they likely won’t have to pay much tax on the payments.

Give us a call if you are thinking about opening a Registered Education Savings Plan (RESP) to save for your child’s post-secondary education? We can help you find the right solution to meet your needs, optimize investment performance and ensure your child has sufficient funds to pay for post-secondary education. Talk to us about RESP today.

THINKING ABOUT OPENING AN RESP FOR YOUR CHILD?

YOU HAVE COME TO THE RIGHT PLACE!

We will help you find the right RESP plan.